By Shaina Cole | Contributing Writer, Rocky Mountain Voice

A familiar promise, a familiar frustration

Voters are often told that a policy includes a built-in safeguard — a cap, a limit, a hard stop designed to keep costs under control. In Colorado, that promise came with the Taxpayer’s Bill of Rights, approved by voters in 1992 as a constitutional amendment limiting how much revenue state and local governments can keep and spend without voter approval. Nationally, it appeared in the Affordable Care Act’s limits on how much of each insurance premium can be kept for administration and profit under the law’s medical loss ratio rules.

The two systems regulate very different things. One governs government revenue, the other private insurance markets.

But critics of both argue they share a deeper similarity: each relies on narrow technical limits that can encourage behavior that complies with the letter of the law while still allowing overall costs to rise.

What TABOR set out to do

Colorado’s Taxpayer’s Bill of Rights amended the state constitution to limit how much revenue governments can retain and spend without voter approval.

TABOR requires elections for new taxes or many tax rate increases and caps retained revenue growth based on inflation plus population growth, a formula outlined by state and local governments and explained by the Colorado Department of Revenue.

When collections exceed that limit, the excess must be refunded to taxpayers unless voters approve otherwise — which is why Coloradans periodically receive TABOR refunds during high-revenue years.

The intent was straightforward: restrain the growth of government and ensure voters, not lawmakers, control tax increases.

Where the pressure points emerged

TABOR’s strictest limits apply to taxes and to revenue counted toward the constitutional cap.

Fees operate differently. In many cases, lawmakers may raise fees without voter approval, and revenue collected by certain government-owned enterprises — entities funded primarily by fees rather than taxes — does not count toward the TABOR revenue limit at all, a distinction explained in Colorado Legislative Council interpretations.

That difference opened the door. When voter approval for taxes is difficult to obtain, policymakers often turn to fees and enterprise structures to fund programs.

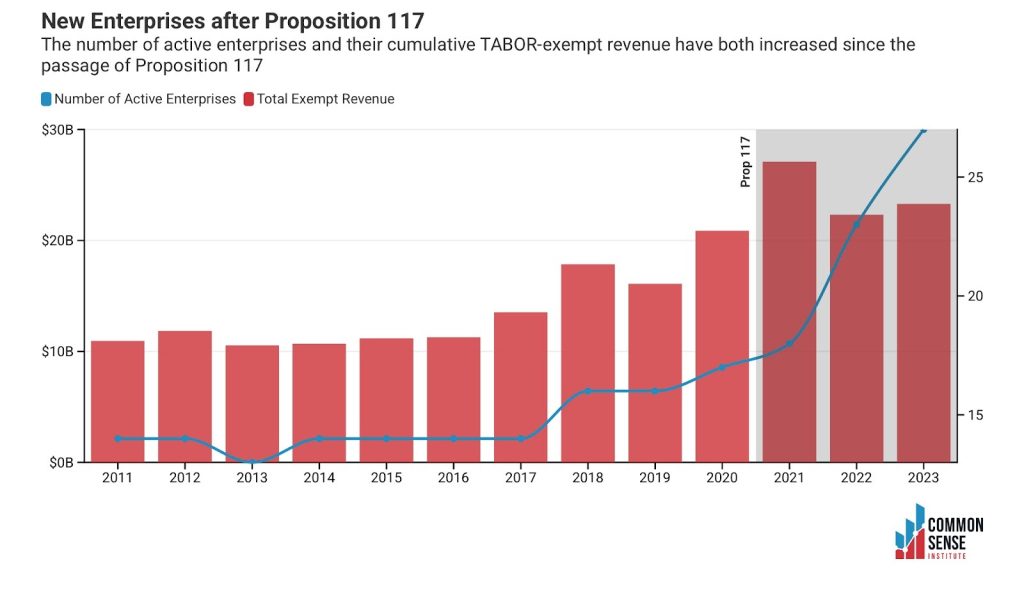

According to research from the Common Sense Institute, revenue flowing through TABOR-exempt enterprises has expanded dramatically since the amendment’s adoption, rising from well under one billion dollars in the early 1990s to more than $25 billion by the 2023–24 fiscal year.

CSI has also documented a sharp increase in the number of state fees over the past decade, alongside substantial growth in combined tax and fee revenue.

In 2020, voters took steps to regain oversight by passing Proposition 117, a measure that requires any new government enterprise projected to generate over $100 million within its first five years to get statewide voter approval.

Afterward, critics — including analysts at the Independence Institute — argued that subsequent legislation, particularly in transportation funding, structured revenue across multiple enterprises or fee programs in ways that avoided triggering a statewide vote.

Supporters of those laws dispute that interpretation, and Proposition 117 itself includes language intended to prevent simple revenue splitting for enterprises serving the same purpose. Even so, the debate highlighted ongoing tension over whether TABOR’s promise of voter control has weakened over time.

Critics quoted by CPR argue that many modern fees function less like payments for specific services and more like broad revenue tools used to fund general policy goals. From that perspective, they contend that the increasing reliance on fees and enterprise revenue has eroded TABOR’s practical effect, even as Colorado continues to advertise comparatively low tax rates.

The ACA’s version of a cap

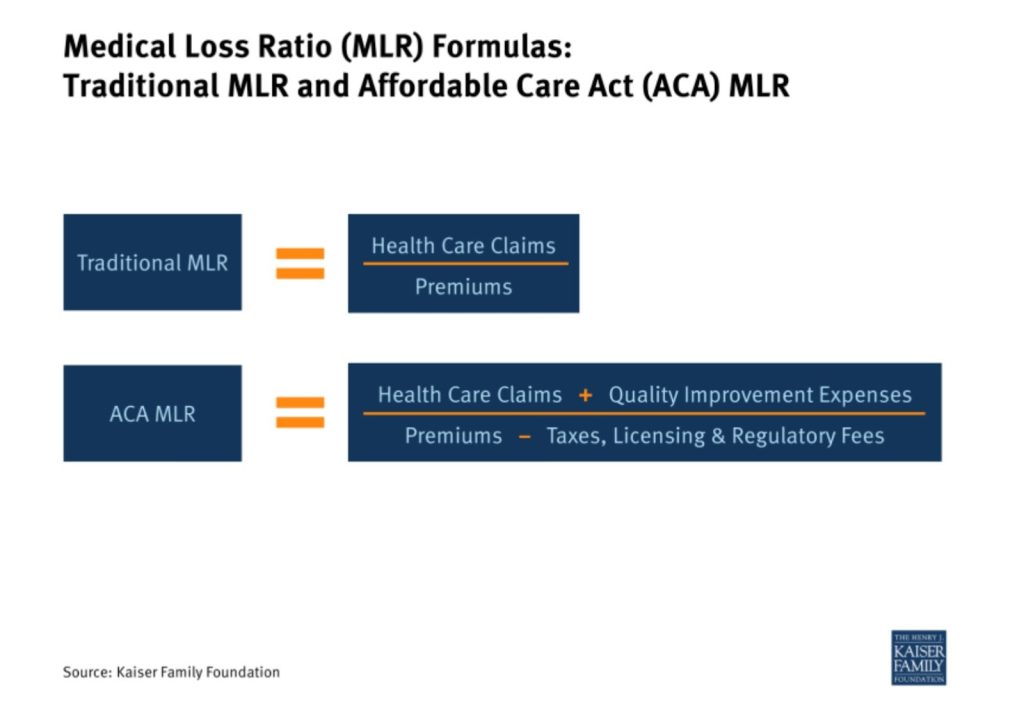

As part of the Affordable Care Act, the medical loss ratio was put in place to protect consumers.

The rule requires insurers to spend 80% or 85%—depending on the plan—on patient care and quality improvements. If they don’t, they are supposed to give the extra money back to customers.

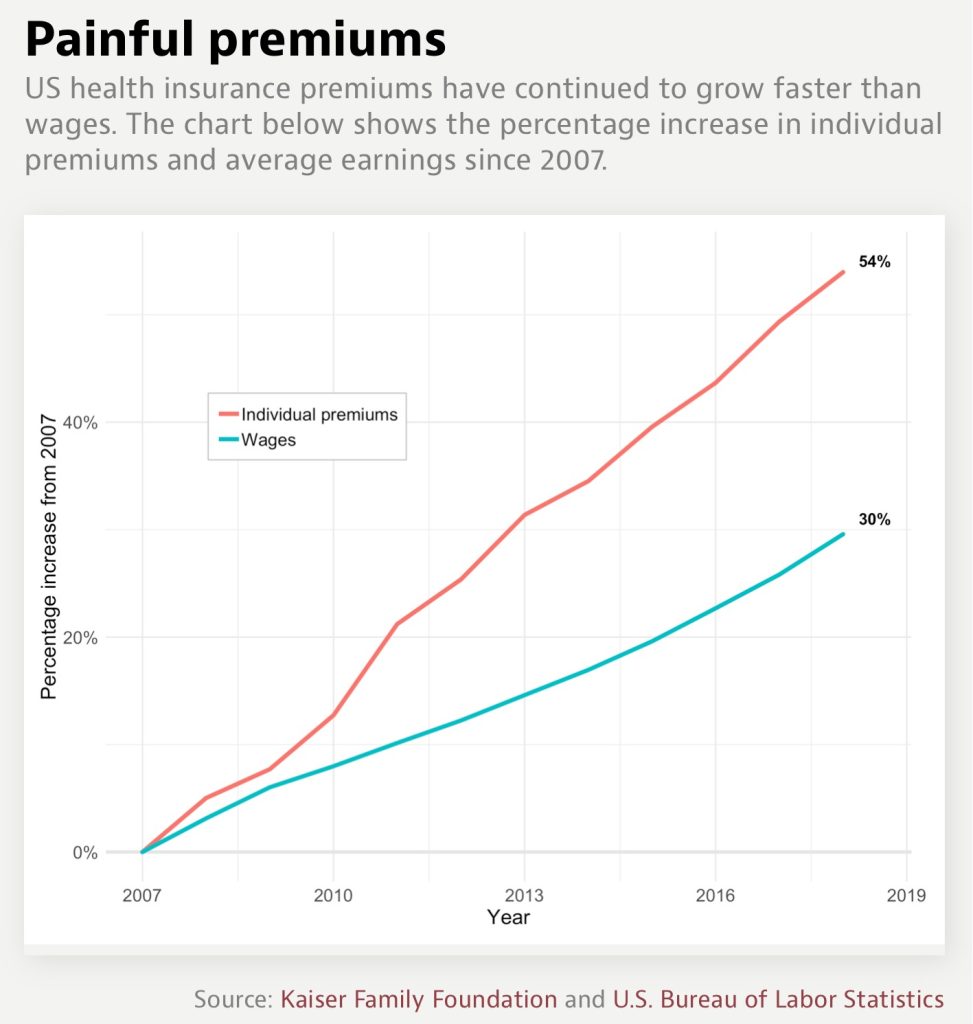

This refund system, calculated over a three-year period, has returned billions to policyholders since the ACA went into effect.

On paper, the rule sounds like a direct limit on profit and overhead. It is often described as the “80/20 rule,” suggesting a hard ceiling on how much insurers can keep.

How incentives shift in practice

The medical loss ratio does not cap premiums themselves. It caps profit and administrative costs as a percentage of premiums, not as a fixed dollar amount — a distinction noted in CMS guidance and health-policy analysis.

That distinction shapes insurer behavior. Economic research published by the American Economic Association found that insurers who initially fell below the required ratios were more likely to increase medical spending than to significantly reduce premiums. Raising claim costs — the numerator in the ratio — was often easier than shrinking premiums — the denominator.

https://www.aeaweb.org/research/regulating-health-insurers-aca-medical-loss-ratio

Since profits are tied to a fixed percentage of premiums, insurers can boost their dollar profits by raising premiums or adding more enrollees, as long as they stay within the 15–20% cap.

As the Kaiser Family Foundation explains, the rule limits administrative spending as a share of premiums, not the premiums themselves, and research summarized by the American Economic Association shows that meeting the requirement has not consistently translated into lower premiums once insurers clear the threshold.

Different systems, similar tensions

TABOR and the ACA were designed to solve different problems. TABOR aimed to restrain government growth and give voters control over taxes. The ACA’s medical loss ratio provision sought to limit insurer overhead and ensure premiums largely fund care.

In both cases, the cap applies to a specific measure rather than to total dollars moving through the system. TABOR limits taxes and retained revenue, but not all fees or enterprise income. The ACA limits profit as a share of premiums, but not premiums themselves.

This setup helps explain why many Coloradans face higher fees even when tax rates stay mostly unchanged — and why insurance premiums can rise even if insurers meet the 80 or 85 percent spending rule. Still, supporters say these rules offer important limits on insurer spending.

Supporters argue the safeguards still provide meaningful constraints. Critics counter that the rules, as written, can quietly reward higher overall costs while maintaining the appearance of restraint.

For voters and consumers, the result often feels familiar: a promise of protection on the front end, followed by confusion when the bill keeps getting bigger anyway.