Cory Gaines | Commentary, Colorado Accountability Project

The two bills linked at bottom (SB26-049 and SB26-155 respectively) present an interesting contrast in policy intended to lower homeowners insurance premiums.

I thought a comparison of the two might be illuminating. It’s not going to be entirely black and white, these aren’t polar opposites, but in looking at the bills together I think you can get a sense of the “legislative style” of those involved.

The fiscal notes of both provide a pretty apt summary, so let’s start there.

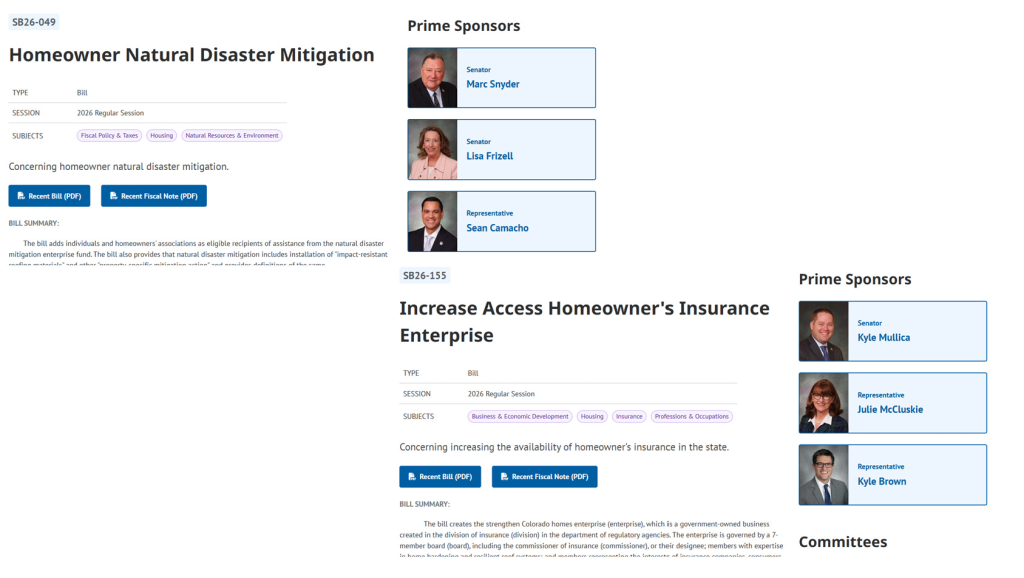

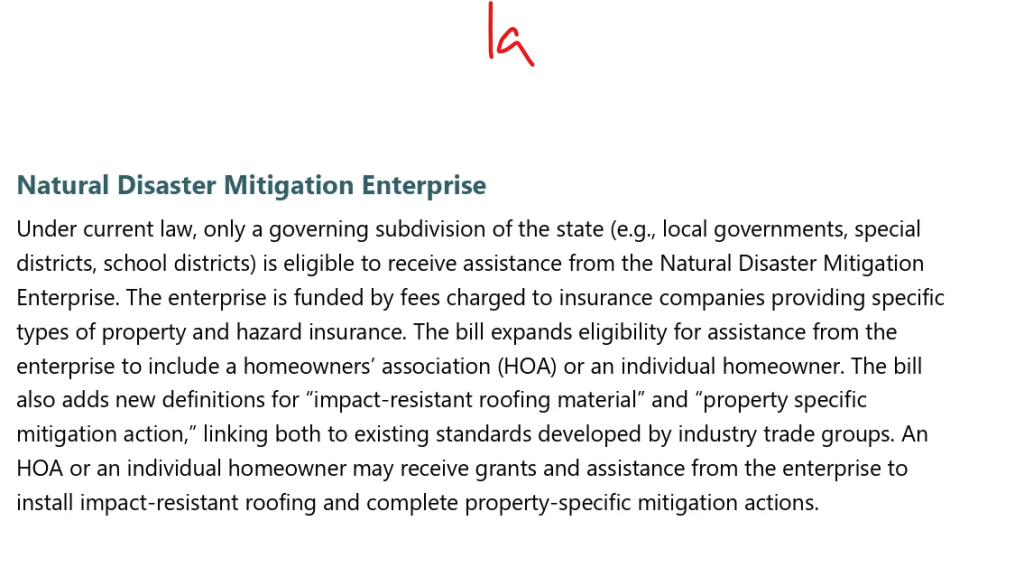

Screenshots 1a and 1b show the summary for SB26-049.

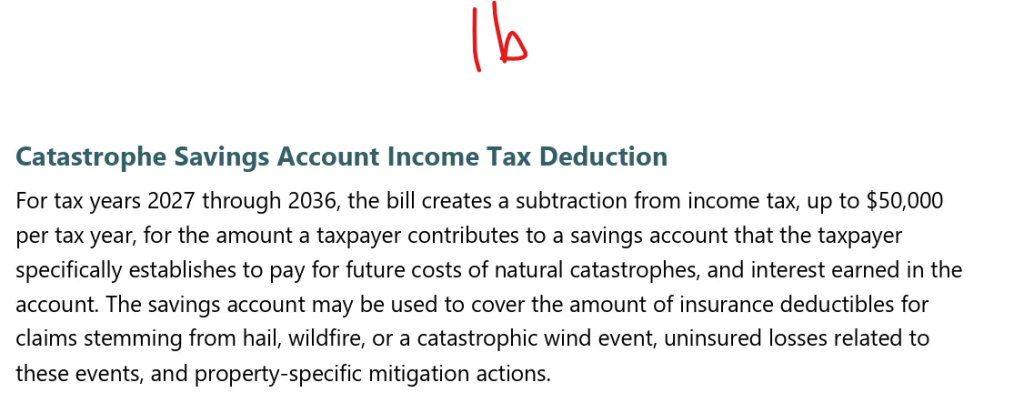

Screenshots 2a and 2b show the summary for SB26-155.

In the former you increase the people who qualify for grants from an existing enterprise as well as creating/incentivizing personal savings for disaster mitigation.

In the latter you make an entirely new enterprise, with another unelected board, to hand out grants to people. The grants are funded by a new fee on homeowners insurance companies.

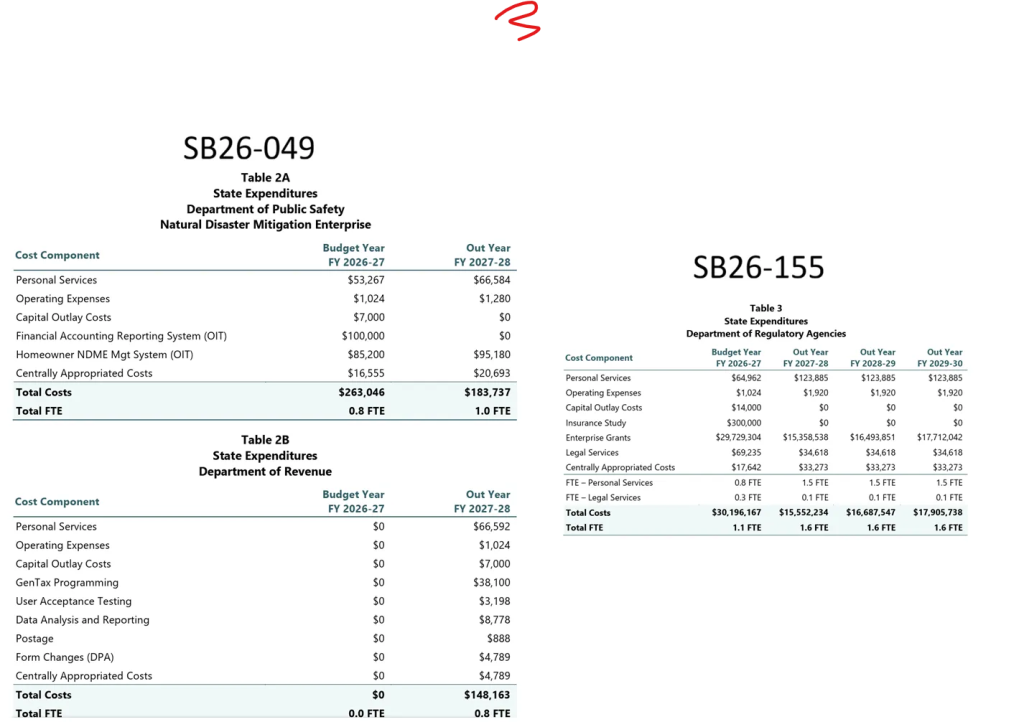

What the bills are set up to do is one thing, what effect they have on our state government is another. Screenshot 3 attached is a side-by-side comparison of estimated increases in state expenditures for the two bills.

Clearly SB26-049 has a much lighter impact; it doesn’t cost as much and doesn’t grow government as much. SB26-155, in comparison, grows it considerably.

This is not a black and white comparison. You do not have one bill based on principles of liberty and personal choice/responsibility vs. one that is all government interventionism and wealth transfer. A look at the pictures of the sponsors should explain why SB26-049 is not the polar opposite of SB26-155; there are a couple government sponsors and (from what I hear) a rather “squishy” Republican sponsor.

Still, if I had to pick, it’d be SB26-049.

I’d rather have neither as they stand right now, but given the choice, I’m almost always going to be behind less (frankly unnecessary) government intervention. There are already discounts and incentives built into homeowners plans to encourage people to be responsible because insurance companies know that responsible choices reduce claims.

SB26-049 works with those incentives and encourages people to be responsible. SB26-155 shifts the burden to the government and makes us all pay for the choices others make.

Sooner or later, if we want to have any sort of economy left in this state, we have to break from the idea that government intervention makes things cheaper. That taking from some to give to others will help us all. We need to encourage more self-reliance, more cognizance of how your decisions about where and how you live play out in terms of risk, and more responsible decision-making.

We cannot continue to make everyone in the state financially responsible for how others choose to live. Doing so only means more government dependence.

From the bill’s summary: “The insurer shall not surcharge the fee amount to policyholders.” Indeed. That is in SB26-155. What this means is that this fee placed on homeowners insurance cannot explicitly appear on your bill. Let’s not all be naive, however, in thinking that the homeowners insurance companies will eat the cost. According to the bill’s fiscal note, in 2024 insurers reported $5.2 billion in homeowners premiums collected. If we assume, at least in the first year, the bill’s 0.5% fee, that would mean insurers would eat $26 million in fees to the state.

Not. Bloody. Likely.

What will most likely happen is that the fee will be passed to customers, it just won’t appear on a bill.

I contacted Senator Mullica’s office to try and clear up this confusion. I was promised a call back but didn’t receive it as of this writing.

https://leg.colorado.gov/bills/SB26-049

https://leg.colorado.gov/bills/SB26-155

Related:

Re. the SB26-155 linked in the post above, Sun reporter (see the first link) Jesse Aaron Paul had this to say:

“The fee would be allowed to generate up to $100 million in its first five fiscal years, and insurance companies would be prohibited from passing the cost on to consumers.”

CPR’s Bente Birkeland had this to say about that same topic (see the second link):

“[State Senator Kyle] Mullica came on board to sponsor this year’s bill, after he joined with Republicans to help defeat a similar proposal last session because he worried insurance companies would pass the fee directly to consumers. This year’s version says the ‘insurer shall not surcharge the fee amount to policyholders.’ It’s not yet clear how that may be enforced.”

Quite a difference and the comparison demonstrates the tilt of the Sun, all the more so when you note that CPR ain’t exactly conservative-leaning.

https://coloradosun.com/2026/04/14/colorado-fees-legislature-strategy-change/

https://www.cpr.org/2026/04/07/colorado-bill-lower-homeowners-insurance-rates-weather/

State Title Board denies title for the transparency amendment

Per the CFOIC article linked at bottom the State Title Board voted at last Wednesday’s meeting to deny title to the transparency amendment that would enshrine the people’s right to know in the State Constitution.

I’ll leave it to you to read up on the details if you like. I don’t think the measure will be dropped, but it may get some changes or a re-hearing may be requested.

I heard that the folks supporting this measure plan to appeal later this week. I’ll update as I know more about that.

In the meantime, I took a minute to send a (belated, but I hope not too late) email to the State Title Board urging them to reconsider.

READ THE FULL COMMENTARY AT COLORADO ACCOUNTABILITY PROJECT

Editor’s note: Opinions expressed in commentary pieces are those of the author and do not necessarily reflect the opinions of the management of the Rocky Mountain Voice, but even so we support the constitutional right of the author to express those opinions.