By Shaina Cole | Contributing Writer, Rocky Mountain Voice

Rep. Yara Zokaie stood before the House Finance Committee on March 9 and made the case for HB26-1221, a bill targeting executive pay deductions and corporate loss carry-forwards. “Our families are struggling to juggle their rent, groceries, and utilities,” she said. The legislature had a choice. It could “choose to protect tax breaks for millionaire CEO salaries” or “allow for a break for our hard-working Coloradan families.”

Zokaie also co-signed HB26-1289. The reengrossed text of that bill, passed by the House on May 4, contains a provision requiring Colorado workers to add their federally exempt overtime pay back into state taxable income. Congress created a federal income tax deduction on overtime pay — up to $12,500 per worker annually, through 2028.

That contradiction runs through a four-bill package now heading to the Colorado Senate with days left in the legislative session.

The bills raise taxes on Colorado businesses by an amount the Colorado Chamber of Commerce estimates at close to 50 percent of the state’s current corporate income tax base. A base that raised roughly $1 billion in 2025, according to Patrick Boyle of the Colorado Competitive Council during hearing testimony.

The revenue funds a new Family Affordability Credit for low-income parents with children. It takes from corporations and gives to struggling families.

When businesses absorb a tax increase of this scale, the costs don’t stay on corporate balance sheets. They move — into prices, wages, hiring decisions, and in some cases, the decision to leave.

If we choose to protect tax breaks

Rep. Karen McCormick opened the HB26-1222 hearing by describing what HR1 had done to Colorado. It “reduced taxes for big businesses in Colorado to the tune of $1 billion last year and at the same time blew a billion dollar hole in our budget,” she told the committee.

Her co-prime sponsor, Rep. Lorena Garcia, described families who couldn’t count on “what else is going to come down from the federal administration” from one day to the next. The package, Garcia said, was a chance to “make something permanent for families.”

The four bills are built on that argument.

HB26-1221, sponsored by Zokaie and Rep. Emily Sirota, caps the state deduction for executive compensation from $1 million to $250,000 per executive and limits how far corporations can carry business losses forward — from 20 years to 10, and from 80 percent of taxable income to 70 percent.

HB26-1222 disconnects Colorado from four federal deductions for equipment purchases, manufacturing buildings, research costs, and business interest expenses. Companies still claim those deductions on federal returns. At the state level, they must now maintain separate tracking schedules for each — in some cases for up to 38 years per asset.

HB26-1223, sponsored by Reps. Steven Woodrow and Andrew Boesenecker, ends a 2012 sales tax exemption for downloaded software, apps, and subscriptions.

HB26-1289, sponsored by Garcia and Rep. Kyle Brown, contains the overtime add-back along with changes to enterprise zone credits, opportunity zone treatment, and vendor allowances.

The revenue from all four funds the Extended Family Affordability Credit.

Under the bill, the credit amount is not fixed. Legislative Council Staff calculates it each December based on projected revenue, then sets a per-child amount so total credits paid out match total revenue raised.

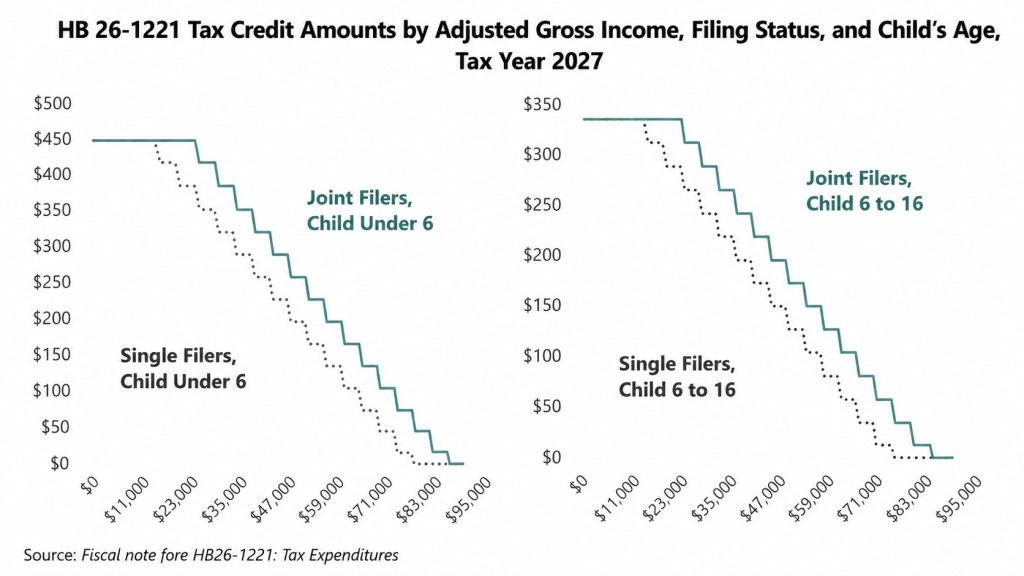

The new credit’s income structure mirrors its predecessor, the Family Affordability Tax Credit. In tax year 2024, 320,490 Colorado households claimed it. The new credit’s maximum is less than 15 percent of what families received then.

Legislative Council Staff sets the per-child amount each December based on projected revenue. For tax year 2027, the HB26-1221 fiscal note projects a maximum of $443 per child under six for the lowest-income single filers and $332 for joint filers. The amounts adjust each year based on how much revenue the bill’s business tax provisions actually raise.

According to the federal Administration for Children and Families’ 2025 Child Care Market Rate Survey, center-based infant care in Colorado averages $1,600 per month. The maximum estimated credit covers roughly one week of it.

Where the cost lands

Philip Horwitz came to the hearing as chair of the Colorado Chamber of Commerce Tax Council, having previously served as director of the Office of Tax Policy at the Department of Revenue. He told the committee he understood why previous legislatures had asked businesses to absorb budget pain. “In prior downturns and budget shortfalls, the business community has, if not been happy to bear some of that burden, has certainly been understanding of the need to bear some of that burden…in prior downturns, the net operating loss has been adjusted temporarily as a way to help fund that shortfall. But in this case, we’re not funding that shortfall.”

Patrick Boyle told the committee, “The ultimate question you need to ask yourself is where will your children work and where will your children live? And if we don’t have the kind of tax and regulatory environment that encourages investment here, businesses will vote with their feet and they’ll make their investments in other states.”

He said the burden would fall hardest on multi-state corporations, which he described as having the mobility to act on it.

The Colorado Chamber Foundation’s Relocations Tracker shows 98 companies have left since 2019, taking more than 13,600 jobs — 21 to Texas alone.

Rep. Max Brooks brought up affordability, “Colorado has absolutely become an unaffordable place to live,” Brooks said. “And I don’t know that punishing businesses or individuals that have been successful is the best way to be able, in my opinion, to be able to get to the problem that you’re trying to solve.”

Steve Betts, CFO of Merrick and Company — Colorado’s largest employee-owned engineering firm, with more than 400 of its 1,000 employees working in Colorado — opposed the research deduction change in HB26-1222. “Allowing companies to deduct R&D expenses in the year incurred encourages competition,” he told the committee. “It’s vital to innovation, supports technological advancement, and has been federal policy for over 70 years.”

Decoupling from it does not change what a company deducts federally.

Rep. Bob Marshall, a Democrat on the Finance Committee, raised a contradiction inside the package itself. “When we keep saying tax credits that help the rich, we got [these package EV] credits coming in where 75, 80 percent of the benefit goes to the people in the top 20% of the median income,” he said. “Yet we don’t touch that.” He voted no.

Colorado taxing overtime pay Congress made deductible

When Congress passed the One Big Beautiful Bill Act in July 2025, it eliminated federal income taxes on overtime pay. Because Colorado’s tax code automatically follows federal law, that exemption would have flowed directly to Colorado’s hourly workers.

Governor Polis signed HB25-1296 in 2025 as a one-year measure to block it and protect state revenue for tax year 2026. The Institute on Taxation and Economic Policy estimated that decoupling saved the state $119 million.

That was meant to be temporary. HB26-1289 — the bill Zokaie co-signed — removes the expiration and writes the overtime tax into state statute with no end date. Section 3(u) of the reengrossed text requires Colorado taxpayers to add “the amount of any overtime compensation excluded or deducted from federal gross income” back into state taxable income, effective for income tax years beginning January 1, 2026.

The package decoupled from every HR1 provision that reduced state revenue from businesses. It also decoupled from the one provision that lowered taxes on hourly workers’ paychecks — and now makes that decision permanent.

A nurse working a double shift, a warehouse worker covering for a colleague, a restaurant worker picking up a weekend — if they have no qualifying children, or their income clears the credit threshold, they pay Colorado income tax on every overtime dollar the federal government exempted. Nothing comes back.

Garcia closed the HB26-1222 hearing with this: “When we are addressing those most in need, everyone benefits,” she said. “This is a perfect example of ‘the tide raises all boats.’”

For the roughly 88 percent of Colorado households that don’t qualify for the credit, that tide arrives through the businesses that serve them — in what those businesses charge, what they pay, and whether they.