By Jen Schumann | Rocky Mountain Voice

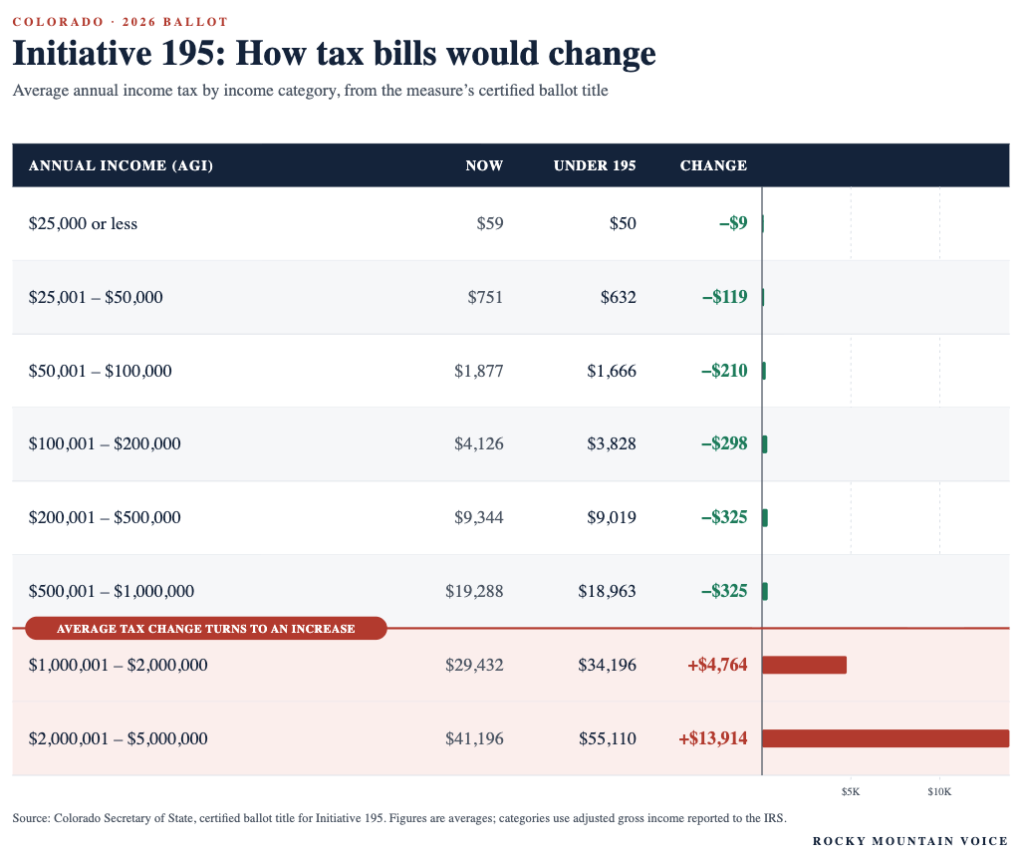

The income tax on a Colorado household earning under $25,000 would fall by $9 a year under Initiative 195. A filer reporting between $2 million and $5 million would pay about $13,914 more. Both figures come from the measure’s certified ballot title.

The Common Sense Institute, a free-market policy group in Greenwood Village, says that second household is also the one most likely to pack up and leave Colorado, and that the state would lose part of the revenue the tax is supposed to bring in right along with it.

Initiative 195 would end Colorado’s flat income tax. The state taxed income on a graduated scale for its first 50 years, then switched in 1987 to a single rate, now 4.4 percent, that applies to every earner.

In its place, 195 would set six brackets, from 3.7 percent on the lowest taxable income to 8.4 percent on income above $1 million, taking effect in tax year 2027. The new rates apply to people, estates, trusts and corporations. Anyone under roughly $500,000 in taxable income would pay the same or less. Above that, the rate rises steeply.

The state puts the increase at up to $2.7 billion a year. The measure earmarks it for K-12 schools, health care, early childhood programs and the Healthy School Meals for All program. Because voters would approve the higher rates, the state could keep and spend the money outside the limits set by the Taxpayer’s Bill of Rights.

Colorado already leans more progressive than its flat rate suggests. The Institute on Taxation and Economic Policy ranks its overall tax code 12th of the 50 states, the product of a large standard deduction and refundable credits that hold down the bottom.

By CSI’s own figures, the 8.4 percent of households making at least $200,000 already pay close to half of all state income tax.

The CSI report, written by fellow Ross Kaminsky and senior research analyst Erik Gamm, projects the new rates would cost the state a net 14 firms and roughly $200 million in corporate profit a year. The top bracket alone would lose an estimated 29 companies that together earn $202 million and employ about 4,200 people.

On the individual side, CSI estimates Colorado would gain about 386 net filers a year, but because the people leaving earn far more than the people arriving, the state would still shed an estimated $186 million in personal income.

CSI built those projections from IRS migration data and academic research on how high earners respond to tax gaps between states. One study it cites, published in the American Sociological Review in 2016, found the wealthy do drift toward lower-tax states when they move, but also that they relocate less often than the general public and that tax-driven flight is small, concentrated almost entirely in moves to Florida.

CSI uses Massachusetts as its closest real-world comparison. Voters approved a surtax on income above $1 million, and the next IRS migration report showed a net loss of nearly 30,000 residents. The Massachusetts Budget and Policy Center, working from the same numbers, has said they do not settle whether the tax drove anyone out.

Closer to home, Colorado business owners have been naming tax and regulatory costs as reasons to leave for months.

In April, RMV reported on Heather Florio, who moved her company to Colorado in early 2025 expecting to stay, then left about seven months later over a change in state tax thresholds she said would roughly double the company’s bill. Her departure had nothing to do with 195, which is not yet law, but it tracks the pressure CSI says the measure would deepen.

The Colorado Chamber’s 2025 relocations tracker logged 27 companies that left, relocated or expanded elsewhere last year, its highest single-year total, and 98 such moves since 2019.

Opponents raise another question the CSI report doesn’t address: how the tax would affect small businesses.

Advance Colorado President Michael Fields argues the proposal would “chase revenue out of the state.” Fields and longtime tax policy advocate Natalie Menten argue the proposal would hit many owner-run businesses particularly hard because they operate as pass-through entities, such as LLCs and S corporations, where business profits flow through to the owner’s personal tax return. They argue that can push even relatively modest firms into the higher tax brackets.

The coalition behind 195, Protect Colorado’s Future, casts it as a response to a state budget hit by revenue caps and federal cuts, including to Medicaid. By the coalition’s count, the measure cuts taxes for 98 percent of Coloradans and raises them only on those earning more than $500,000.

Chris deGruy Kennedy, president of the Bell Policy Center and a coalition member, said an “upside-down tax code” has shortchanged Colorado schools, health care and child care for decades. “Only the voters of Colorado have the power to make the wealthy pay their fair share and restore funding to critical state priorities,” he said.

Backers have until August 3 to collect enough signatures to reach the November ballot. Waiting there is a rival measure, Initiative 232, backed by Advance Colorado, which also opposes 195. It would cap both the individual and corporate income tax rates at 4.4 percent and block the kind of increase 195 proposes.

One measure asks Coloradans to tax their highest earners more. The other asks them to stop the state from ever raising the rate. Both could be on the same ballot.