By Shaina Cole | Contributing Writer, Rocky Mountain Voice

The first-half property tax payment is due every year by the end of February. The number on the front has gone up again. Somewhere near the bottom, a small credit appears: “TABOR credit.”

El Paso County Assessor Mark Flutcher provided RMV with six years of certified tax data for two El Paso County properties: one in downtown Colorado Springs, one in Lorson Ranch, a newer subdivision south of the city.

The numbers show what has happened to Colorado homeowners.

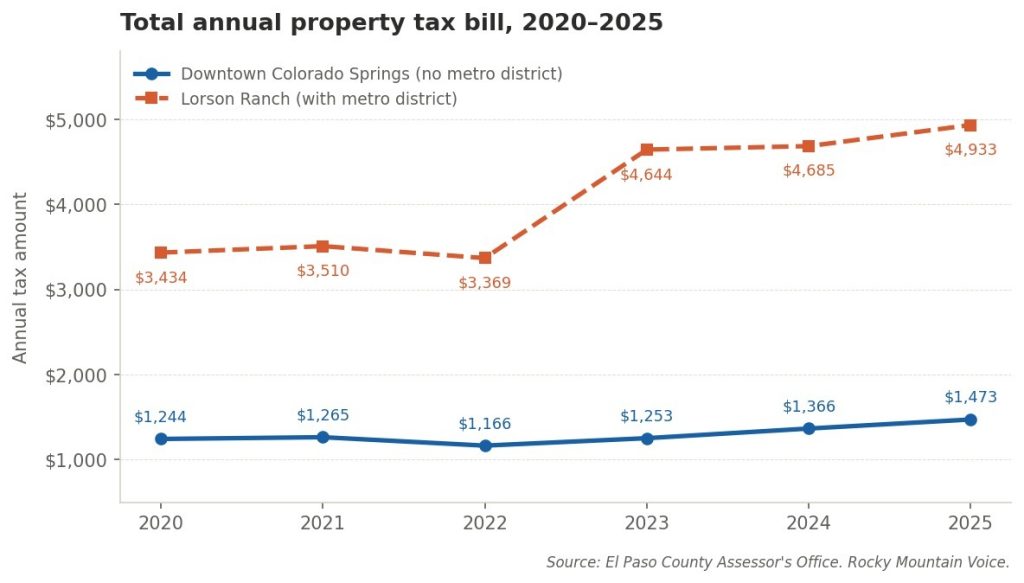

The property tax bill for the downtown home rose from $1,165.61 in 2022 to $1,472.82 in 2025. The Lorson Ranch bill went from $3,369.39 to $4,933.31 over the same period.

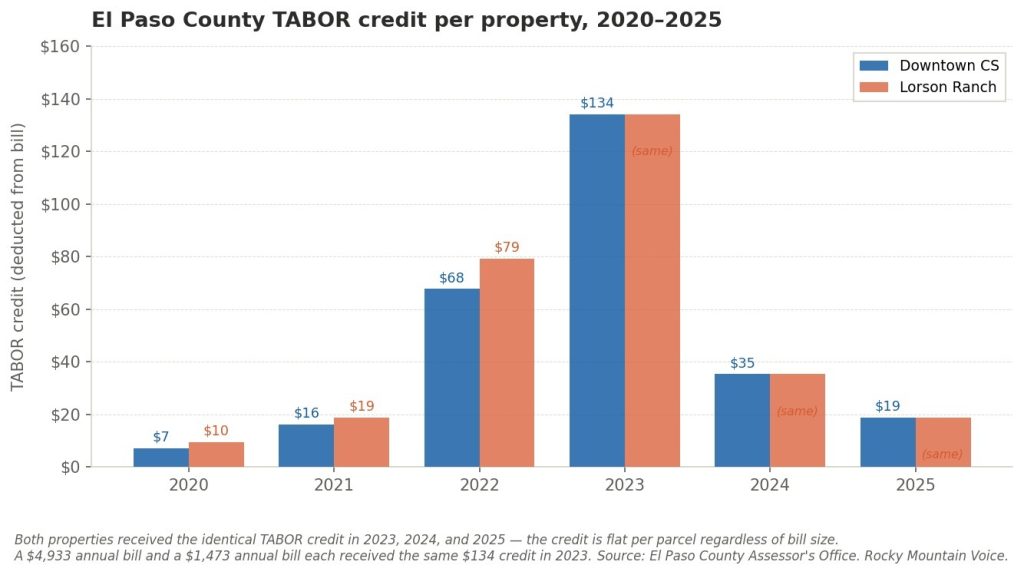

The TABOR credit on both statements, which peaked at $134.08 in 2023, fell to $18.92 in 2025. For the current tax year, it is projected at zero.

Those two trends are not separate stories. They share a cause, and that cause is almost never explained.

Who is actually charging you

Your property tax bill is not a single charge from a single government. It is a stack of charges from every taxing entity that holds a claim on your property. It includes your school district, county, city, fire district, water conservancy and library.

The state sets assessment rates. Each local entity sets its own mill levy. Every line on your statement is a different government that voted to tax you.

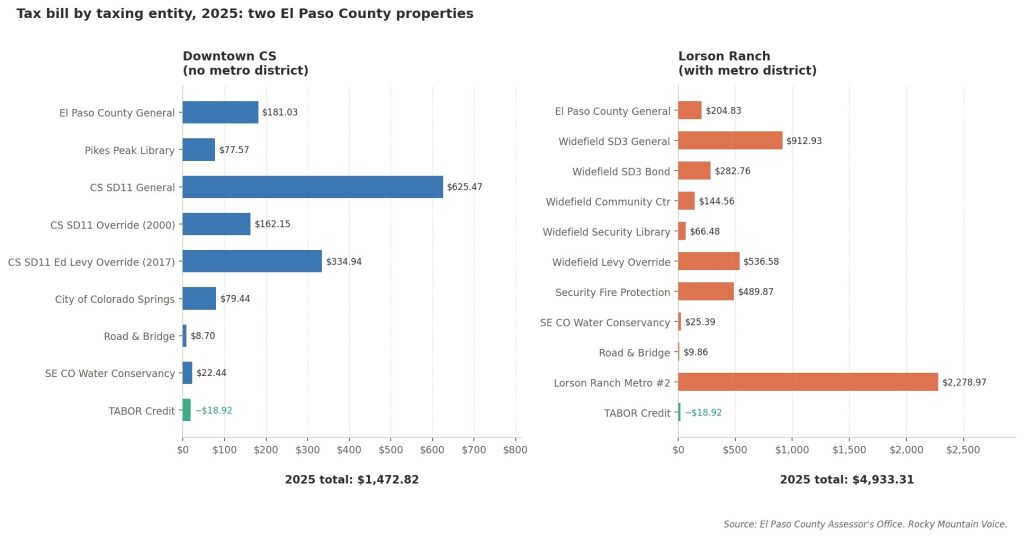

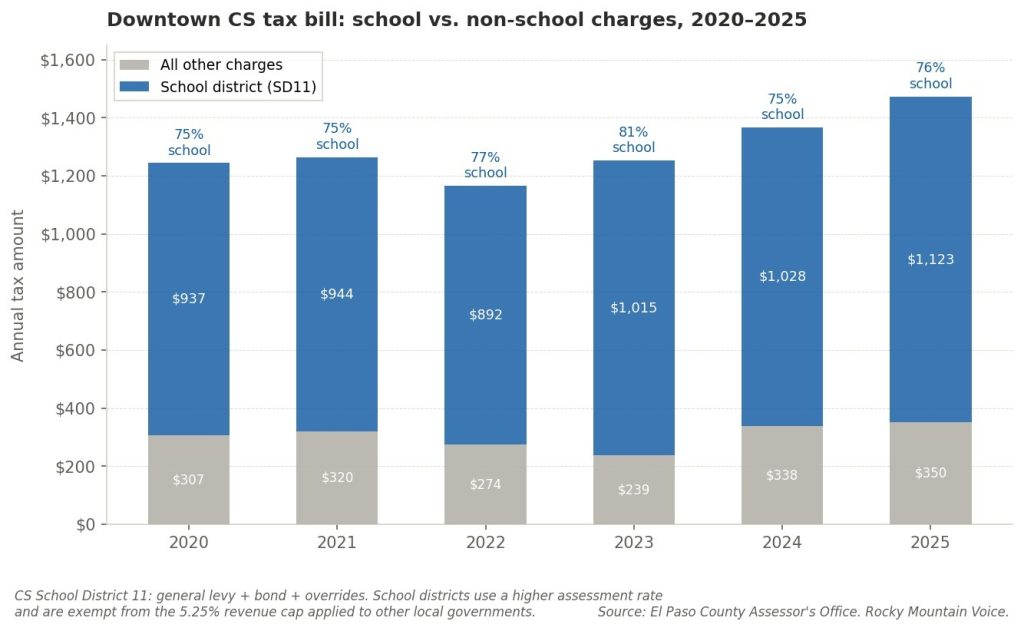

For the downtown Colorado Springs homeowner, the school district is the dominant line.

Colorado Springs School District 11 charged $936.74 in 2020. By 2025 that figure had reached $1,122.56, representing 76 percent of the entire bill. The school district’s share keeps growing because the legislature has given school districts tools that other local governments don’t have.

School districts operate under a higher residential assessment rate than other entities and are subject to a separate revenue limit that does not constrain them the same way the 5.25 percent cap limits what counties, cities, and fire districts can collect. When property values rise, school charges follow without restraint.

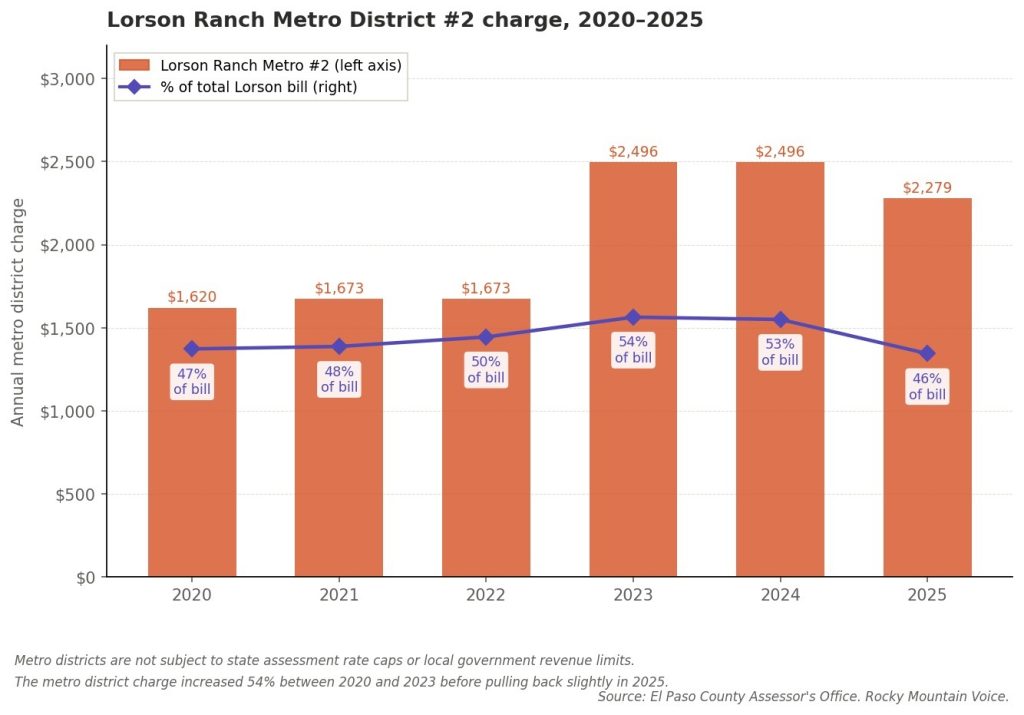

The Lorson Ranch bill tells a different version of the same problem. That property sits inside Lorson Ranch Metro District No. 2, a special taxing entity created by the developer to finance roads and infrastructure before the neighborhood was built.

Metro districts operate outside state assessment rate caps and outside the local government revenue limit. The metro district charged $1,619.78 in 2020, nearly half the total bill. By 2023 it had climbed to $2,495.74. Buyers sign disclosures at closing, but a mill levy buried in paperwork rarely registers until the tax statement arrives.

The 2023 cycle was the worst in recent memory. El Paso County received 33,726 real property appeals that year, more than three and a half times any prior cycle in the data Flutcher provided.

The cause, he told RMV, was structural. “It was a ‘perfect storm’ involving an assessment cycle with ever increasing sales that occurred in 2021 and the first half of 2022. With interest rates increasing after the sales period, values were in decline in 2023.”

State law locks assessors into a specific sales window. By the time bills reflected 2021 and early 2022 prices, the market had already turned.

Flutcher also flagged a less visible variable.

Whether a homeowner absorbed the full brunt of the 2025 assessment rate changes depended partly on whether their local taxing entities had gone to voters to remove their own TABOR spending limits.

For homeowners “in districts that had not de-TABOR’ed,” he wrote, mill levy reductions offset some of the increase. Neighbors can pay meaningfully different bills on similarly valued homes based on a local election most residents never followed.

The refund that shrank

Under Colorado’s Taxpayer’s Bill of Rights, when state revenues exceed a constitutional spending cap, the surplus must go back to taxpayers. For years part of that obligation flowed through counties, which credited it against property tax bills.

In 2022 the downtown homeowner received a $67.76 credit. The Lorson Ranch homeowner received $79.18. Through 2022 the credit scaled with the bill — the larger statement received the larger credit.

Starting in 2023 that changed. The credit became a flat amount per parcel, identical regardless of what you owed. Both properties received exactly $134.08: one on a bill of $1,253.18, the other on a bill of $4,644.24.

The state’s general TABOR refund followed the same arc. For tax year 2023 it reached $800 per filer, for tax year 2024 it fell to $177 and $565, and for tax year 2025 it sits between $19 and $59. For tax year 2026, it is projected at zero.

The hinge that connects them

Under Colorado law, the state reimburses local governments for property tax revenue lost because of the senior, disabled veteran, and Gold Star spouse homestead exemption. That reimbursement is the first obligation paid out of any TABOR surplus, before general refunds reach anyone else.

As property values rose, the exemption became more expensive to cover. The larger that first-priority claim on the surplus, the less left for the general refund. The policy that reduced a qualifying senior’s property tax bill was funded, in part, by reducing the TABOR refund of the neighbor who didn’t qualify.

The legislature also expanded targeted tax credits in recent years, including the Family Affordability Tax Credit and an expanded Earned Income Tax Credit, that draw from the same pool before general refunds are calculated. Each expansion left less for the flat refund that reaches every filer.

What was removed from your statement

There is one more piece of this story, and it came from Flutcher.

In August 2024, the legislature passed HB24B-1001, the special session bill that restructured assessment rates. Tucked inside it were two provisions that took effect for tax year 2025. Assessors were prohibited from showing the assessment ratio on the Notice of Value mailed to homeowners, and treasurers were prohibited from showing the assessed value on the tax statement itself.

Those are the two numbers a homeowner needs to check the math on their own bill. Both were removed by the legislature in the same bill that changed the rates. Assessors got the blame.

Flutcher said his office was accused of “hiding information” and “creating a lack of transparency” once the figures came off documents homeowners had always seen. “In turn, assessors were accused of ‘hiding information’ and ‘creating a lack of transparency.'”

County assessors had no role in that decision. They fielded the calls anyway.

November’s question

This fall, Colorado voters will be asked to let the state keep more of the surplus that produces the credit on their property tax statement.

The ballot question, from SB26-135, frames it as a K-12 investment: two percent more compounded per year for ten years, used to raise teacher pay, improve retention, lower class sizes, and increase access to career and technical courses, “without raising taxes but instead funded by raising the annual limit on state fiscal year spending…”

The word “refund” does not appear in the ballot title.

The bill’s own fiscal note tells the full story. If voters approve, the state would keep $136.1 million in surplus revenue in fiscal year 2026-27 and $969.7 million in 2027-28 that current law requires it to return.

Under the bill’s spending waterfall, homestead property tax exemption reimbursements come before teacher pay or class sizes.

The same mechanism that has been drawing down the TABOR surplus for years is embedded in the measure voters will decide in November.

Colorado Union of Taxpayers president Kim Monson called it a workaround. “This legislation proposes this voter referendum for the purpose of bypassing TABOR limits and allowing the state to keep our TABOR refunds from money that the state over collected in taxes from us,” she told RMV.

The legislature also passed HB26-1419 this session, arguing the state accidentally overpaid $306.1 million in prior-year refunds because of how federal tax changes interacted with Colorado’s accounting. Polis signed it into law on June 3.

The bill authorizes withholding future refunds to recover that amount. Joint Budget Committee staff wrote in a February 20 memo that the refund “does not appear to qualify as an over-refund under current statute,” after consultations with legislative legal, fiscal, and audit staff.

CUT called the bill “an ‘ex-post-facto’ style tax increase.” Monson went further, telling RMV, “The actual return of taxpayer’s money is determined mathematically and not subject to terminology applied.”

The downtown homeowner and the family in Lorson Ranch will both see that question on their ballots.

The downtown bill is up more than $300 since 2022. The Lorson Ranch bill is up more than $1,500.

Their TABOR credit has gone from $134 to less than $19. They will be asked, without the word “refund” anywhere in the question, whether to give up what remains.

![FD863768-0ACF-495E-9D21-2EF784DFFA6B[1]](https://rockymountainvoice.com/wp-content/uploads/2026/06/FD863768-0ACF-495E-9D21-2EF784DFFA6B1-300x300.png)