By Cory Gaines | Commentary, Colorado Accountability Project

Rising homeowners insurance rates have been a hot topic at the capitol this legislative session. I wrote about a couple bills to do so in late April. That newsletter is linked first below.

It wasn’t too long after writing about this laser focus on homeowners insurance affordability by our legislature that I finally had a free minute to comparison shop on mine.

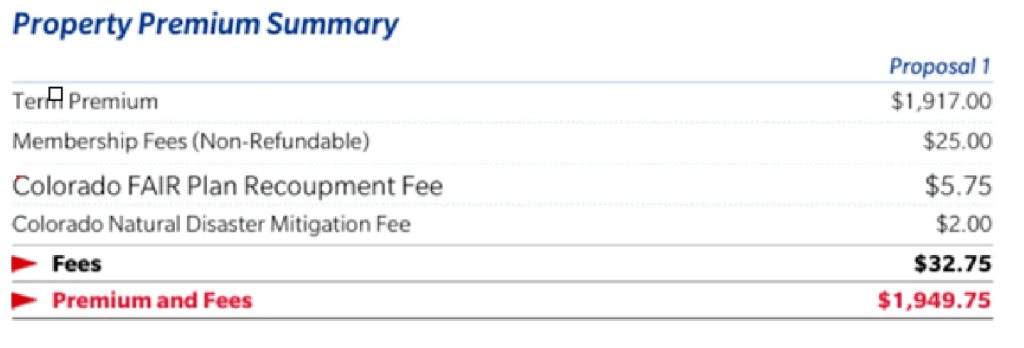

The picture heading this post is from one of the quotes I got. While the legislators talk a great game about affordability, right there on the quote are two brand spanking new fees they imposed. Let’s look at what they are.

The first is a $5.75 (yearly) fee assessed on my insurance: a Colorado FAIR Plan Recoupment Fee.

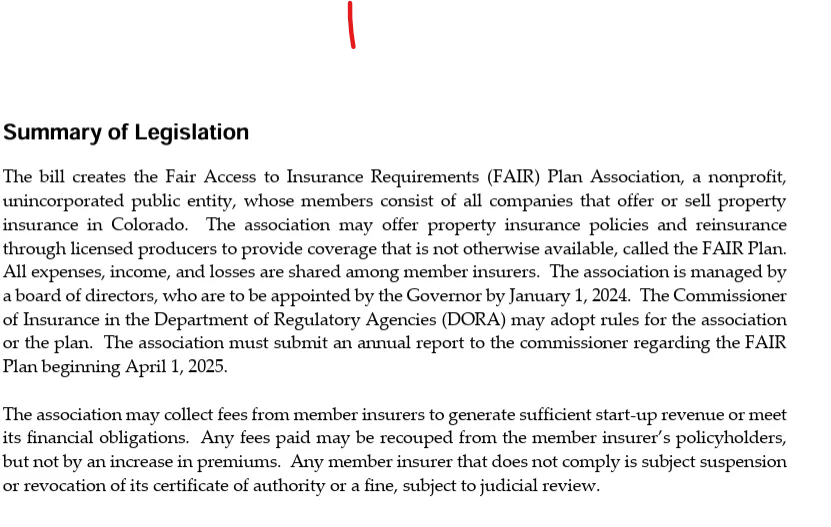

This program — FAIR standing for “fair access to insurance requirements” — was created by a 2023 bill which I link to second below. The bill passed, got signed, and is now an officially up and running government program. The program’s website is linked third.

What are we paying for? Screenshot 1 attached is from the bill’s fiscal note and provides a summary, but it’s not too hard to quickly describe. It’s partial subsidization for some on the backs of others.

The bill creates a group composed of any business selling property insurance in Colorado. This group is tasked with creating a backstop plan to provide property hazard insurance to folks in Colorado who normally couldn’t get it. All the businesses decide on what is in this special insurance plan, pool their resources, and share costs/profits/losses together. Unless, of course, there’s not enough to meet the financial obligations.

Said another way, policyholders like me (and you when you update your insurance) are paying to start up this program and we are the ultimate backstop. We pay more so the insurance companies can sell to people they wouldn’t have otherwise and still feel safe knowing a disaster won’t hit them.

I had to laugh when I saw this particular line from the fiscal note: “Any fees paid may be recouped from the member insurer’s policyholders, but not by an increase in premiums.” Good lord, do any of the sponsors or people who voted for this think that makes a difference to my wallet?

Why am I being asked to help fund other people’s choices? Do I get any benefit from it? If someone builds in the wilderness and can’t get homeowners insurance because of it, do I get to sleep in their guest room on vacation?

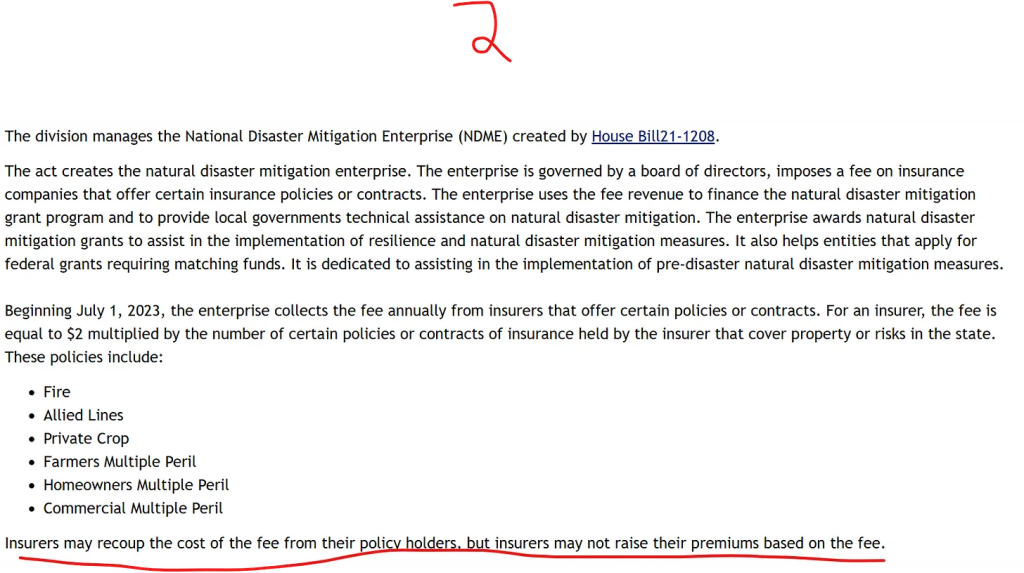

The second fee, the $2 Colorado Natural Disaster Mitigation Fee, is from a 2021 bill which I link to fourth below. What are we getting for this? Besides getting another unelected enterprise which is enabled to collect fees from us all, I mean.

Screenshot 2 comes from the fifth link below, the enterprise’s site. It details what the program is for and what the money gets spent on. It’s grants going to various places around the state to help mitigate various potential disasters. Oh, and as before, the bill sponsors were kind enough to conserve their talking points about not driving up premiums. You see, insurers can pass this along to you, they just can’t raise your premiums to do it.

Perhaps more than for the first bill, I can see how this one has a rationale. The idea being that preventing or mitigating disasters will result in less insurance payouts and lower premiums (though I’ll believe the latter when I see it).

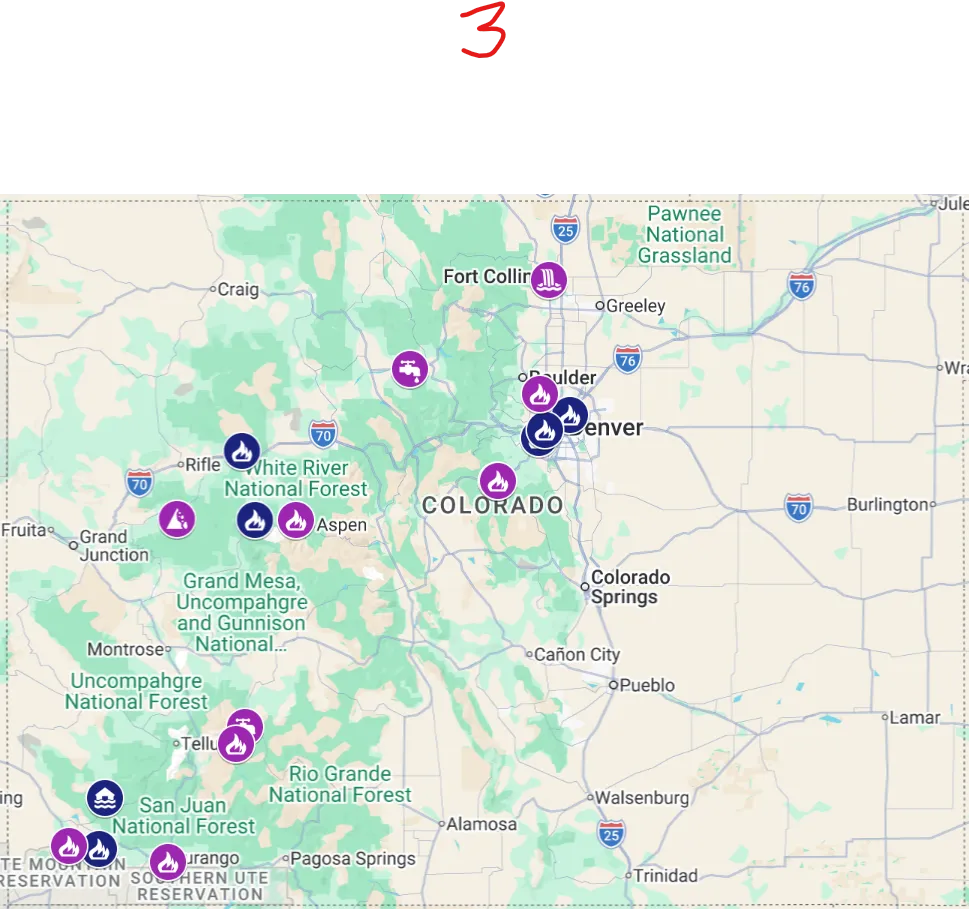

The thing is, if you go and look at the map of grant recipients, screenshot 3 from the sixth link below, you note a decided pattern: there’s a whole lot of the state that does not receive funding. Whether this is due to them not applying or not getting grants, the pattern stands.

One of the fundamental assumptions that let our state supreme court say that government enterprises charging fees were not the same as taxes (and thus exempt from TABOR) was their contention that an enterprise is a business accepting fees for services; that is, you pay and receive a benefit from the enterprise.

If you live anywhere NOT getting money, you’re still paying, but what benefit do you receive? While I like the idea behind the program, I think there is a fundamental flaw in this bill. This should not be a statewide enterprise. Otherwise you have a situation where I, way out here in Logan, or you, down there in Pueblo, are paying for Fort Collins to have fewer disasters. There’s little to no reason to think that preventing disasters there will affect the actuarial tables for where I (or you) live.

In the post that follows this one today, we’ll see how this sort of reasoning–that you and I and everyone else need to subsidize things for others via higher fees–is alive and well in our state legislature in the current session.

**At my last check, both were awaiting further hearings either to get out of one chamber or past a committee in another. Bill links are in the newsletter if you’re curious.

https://coloradoaccountabilityproject.substack.com/p/comparing-two-bills-intended-to-lower

https://leg.colorado.gov/bills/hb23-1288

https://leg.colorado.gov/bills/hb21-1208

https://dhsem.colorado.gov/NDME

https://dhsem.colorado.gov/NDMEmap

READ THE FULL COMMENTARY AT COLORADO ACCOUNTABILITY PROJECT

Editor’s note: Opinions expressed in commentary pieces are those of the author and do not necessarily reflect the opinions of the management of the Rocky Mountain Voice, but even so we support the constitutional right of the author to express those opinions.